Docket W01302

Order W92-4IN THE MATTER of an application of the Charlottetown Water Commission dated July 22, 1991.

BEFORE THE COMMISSION

on Wednesday, the 29th day of April, 1992.

Linda Webber, Chairman

John L. Blakney, Vice-Chairman

Michael Ryan, Commissioner

Order

Contents

Appearances & Witnesses

Reasons for Order

Part One—The Application

1.1 Introduction

1.2 The Applicant

Part Two—Revenue Requirement

2.1 Introduction

2.2 Sales Forecast

2.3 Accounting Matters

2.3.1 Introduction

2.3.2 Treatment of Capital Assets—Capital Recovery and Depreciation

2.4 Rate of Return

2.5 Operating Expenses

2.6 Overall Revenue Requirement

Part Three—Proposed Rates

3.1 Introduction

3.2 Cost Allocation

3.3 Rate Design

3.4 Other Matters

3.5 Disposition

Order

Schedule 1

Appearances & Witnesses

1. For the Charlottetown Water Commission

Counsel:

David H. JenkinsWitnesses:

Guy Stewart, Chairman

R.T. Clark, General Manager

D.G. MacLeod, Secretary-Treasurer

J.M. Mulligan, Auditor & Consultant

Michael Loudon, Consultant2. For the Association of Licensed Community Care Facilities

Witness:

Joe McQuaid, President3. For the Island Regulatory and Appeals Commission

Counsel:

Thomas A. MathesonIndependent Witness:

Gerard FitzpatrickStaff:

Donald G. Sutherland, Director, Utilities Division

Heather Walker, Recording Secretary

Reasons for Order

Part One

The Application

1.1 Introduction

This is an application under the Water and Sewerage Act, R.S.P.E.I. 1988, Cap. W-2, by the Commissioners of Sewers and Water Supply (hereinafter referred to as the "Charlottetown Water Commission", the "CWC", "Applicant" or "Utility"). The CWC seeks the approval of The Island Regulatory and Appeals Commission ("Commission") for an amended rate schedule ("Tariff") for the supplying of water and sewerage disposal services for customers in the Utility's service area. The CWC's proposals represent an average increase in customer rates of approximately 63 percent. The present CWC Tariff has been in effect since 1981.

The CWC's application in this matter was initially filed with the PEI Public Utilities Commission ("PUC") on July 22, 1991. In addition to the filing made with the PUC, copies of the application were circulated by the CWC to municipalities in the Charlottetown region potentially affected by the application. On August 1, 1991, the Community of Hillsborough Park filed— through counsel—interrogatories. However, the Community did not formally intervene in the proceeding.

On August 16, 1992, the Community of Sherwood indicated its intention to intervene and, by letter dated September 6, 1991, the Community posed certain questions to the CWC. In addition, on September 18, 1991, Commission staff directed interrogatories to the Applicant. These interrogatories along with the questions posed by Sherwood were answered by the CWC on October 1, 1991.

The public hearing of this matter originally commenced on October 8, 1991 before the PUC. With the consent of the Applicant, the matter was transferred to this Commission—which replaced the PUC on November 4, 1991—and the public hearings were conducted on December 3, 9, 10, 11, 12, 13 and 16, 1991. A written summation by the CWC was filed with the Commission on December 18, 1991. Although a representative of the Community of Sherwood attended the hearings, Sherwood did not actively participate in the hearing process.

The P.E.I. Association of Licensed Community Care Facilities was represented at the hearing by Joe McQuaid, its President. The Association made a presentation on the proposal of the CWC to directly charge customers with unmetered fire lines. A review of this matter is contained later in these Reasons.

In addition to witnesses from the CWC and the presentation of Mr. McQuaid, the Commission heard from Gerard Fitzpatrick, a chartered accountant engaged by Commission staff to give independent evidence on accounting and rate-of-return related matters. The report of Mr. Fitzpatrick was filed on November 12, 1991.

The Commission acknowledges the contributions of all of the participants in this proceeding.

1.2 The Applicant

The Applicant is a public utility within the meaning of the Water and Sewerage Act engaged in constructing, altering, extending, managing and controlling a system for providing water and sanitary sewage disposal services. The CWC is comprised of three part-time Commissioners who are elected to office by residents of the City of Charlottetown. Although the CWC provides services beyond the corporate limits of the City, its membership does not include representation from other municipalities in the provincial-capital region serviced either in whole or in part by the Utility.

The CWC came into existence in the late 19th century with the passing of the Charlottetown Waterworks Act of 1887 and the Charlottetown Sewerage Act of 1898. The following evidence of the CWC's Chairman, Guy Stewart, gives some background on the Utility:

The mandate of the Charlottetown Water Commission is set out in its incorporating legislation, enacted in the year 1887: To supply within the City of Charlottetown on behalf of the citizens of the City pure and wholesome water for domestic fire protection and other purposes, and to build, construct and operate the waterworks. By this legislation, the Commission is vested with the responsibility and authority to consider and decide all matters relating to supplying the City with a sufficient quantity of pure and wholesome water for the use of the City and its inhabitants for all purposes, and the related construction of waterworks. In 1898, this initial mandate was extended by legislation to include authority and responsibility to construct and operate a sewerage system for Charlottetown. This continues to be the primary mandate of the Commission.

In addition, the Commission is authorized to, and does, provide water service to some municipal and individual customers outside Charlottetown. The Commission views as its extended mandate the provision of water service on a bulk basis to municipalities outside Charlottetown and continuation, where necessary, of service to customers outside Charlottetown.

The Commission provides sewerage service outside Charlottetown to the Hillsborough Development1 and Queen Elizabeth Hospital and Riverside Hospital. The Commission cooperates with municipalities in the Charlottetown Area under the auspices of the Charlottetown Area Pollution Control Commission toward the provision of sewerage service to municipalities in the Charlottetown region.

...

The Commission is in the process of becoming the supplier of water in bulk for the greater Charlottetown area. In 1988, the Commission submitted a proposal to the Government of Prince Edward Island, the City of Charlottetown and neighboring municipalities. The Commission has kept the Public Utilities Commission informed of its proposal. Under this proposal, the Commission would supply community water authorities who would provide their own distribution systems. The objectives of this endeavor are consistent with the Commission's mandate of providing security of adequate and pure water supply and the development of an appropriate management scheme with the minimum attendant bureaucracy. This endeavor involves only an extension of existing services provided by the Commission.

The need for new water supply is a priority with the Commission. Two options exist: (1) the redevelopment of the Malpeque Pumping Station to serve the future needs of the citizens of Charlottetown; and (2) the development of the Winter River Basin area for the future needs of the Greater Charlottetown Area. The Commission believes that the long-term solution is option two.

The Commission has indicated to all involved in the bulk service proposal that the Commission's primary responsibility is for the provision of water for the citizens of Charlottetown. It is well understood that the Commission will not allow the development of bulk service for outside customers to be subsidized by the citizens of Charlottetown. The Commission has emphasized that it is prepared to pay its fair share for future supply, but other municipalities must be prepared to pay their fair share. The cost for development of new supply must be recovered through rates and charges approved by the [Island Regulatory and Appeals Commission]. Any funding through Government grants would certainly have an ameliorating effect on the rates and charges.

The Commission no longer entertains requests for new individual service outside the Charlottetown - Hillsborough Development service area, until such time as new supply is available.2

The matter of a new source of supply is not an issue the CWC has now placed before the Commission for review. According to CWC witness Clark:

The long-term plan for increased capacity is the [CWC] proposal to Government to be the bulk supplier for the Charlottetown area. This will serve also to provide security of supply for the citizens of Charlottetown. For future expansion, 80-90% of costs would be related to transmission. On that basis, it is considered cost effective to develop in the Winter River Basin with 2/3 of supply designated for the outside municipalities and 1/3 for Charlottetown. The estimated aggregate capital expenditure for new supply is approximately $3 million ('91) to be borne by classes of customers based on cost and projected usage. The Commission does not seek regulatory approval of this project at this time.3

The CWC does, however, seek within the context of its expenditure program forecast, authority to proceed with well exploration and land acquisition in the years 1992-1993. A discussion on this issue is contained later in these reasons.

The CWC's water system is comprised of three water supply sources, one of which—the Malpeque station—is maintained on standby. The other two sources—the Brackley and Union pumping stations—have a present sustainable safe-yield rating of approximately 1.1 billion gallons per year.

The CWC operates and maintains some 112 kM of water transmission and distribution plant in the Charlottetown region as well as a sanitary sewage collection system. The CWC is a member of the Charlottetown Area Pollution Control Commission ("CAPCC"), a public utility that provides regional sewage collection and treatment services. The CWC manages the CAPCC under contract. The Utility has some 4,800 water customers, 4,600 sanitary sewage customers and a staff complement of twenty-four.

In what follows, the Commission will review the revenue requirement aspects of the application followed by a review of the proposed amendments to the CWC Tariff.

Part Two

Revenue Requirement

2.1 Introduction

The revenue requirement of the CWC constitutes the total dollars considered necessary in a particular accounting period to allow the Utility to provide reasonable and adequate service and facilities. In this case, the CWC calculates its proposed revenue requirement using the simple average of its 1991-1992 operating forecast. This amounts to an average proposed revenue requirement for each of the years 1992 and 1993 of $2,662,263. Revenues in 1990 totaled $1,876,597 and, in 1989, $1,883,488.

Under the Applicant's present cash-needs method of accounting, it incurred a deficit of $232,665 in 1990 and an erosion in its level of retained or surplus earnings from $718,719 in 1989 to $486,124 in 1990. The Applicant projects that its 1991 retained earnings will further reduce to $53,700.

Matters affecting the CWC's revenue requirement include the level of sales forecast in the test period, the accounting methodology used in determining the proposed expenditure level and the expenditures themselves. A discussion on these issues follows.

2.2 Sales Forecast

A Utility's sales forecast impacts on the cost of providing service to the consumer. Costs such as pumping, maintenance and associated supplies are directly affected by a utility's output. In addition, capital requirements and capital-related costs are directly affected by customer demand.

An understatement of a utility's sales forecast will usually result in excessive rates as well as revenues surplus to the needs of a utility. Similarly, an overstatement can result in inadequate rates and a revenue shortfall. It is essential, therefore, that critical attention be paid to a utility's forecast level of sales.

The Applicant's sales forecast in this application deals with the test period 1992/93. Figure 1 shows actual sales and pumpage data from 1981 to 1990 as well as the CWC forecast.

Figure 1

Figure 1 shows that sales within Charlottetown have declined over the last decade whereas sales to customers outside of Charlottetown have increased. According to Mr. Clark:

There has been a shift in usage from inside to outside customers. In 1981, 84% of pumpage went to inside customers, 4% to outside customers and 12% was unaccounted for. By 1990, the UFW4 was 11%, the inside usage dropped by 12% and outside customers has [sic] increased to 17%. Part of the shift is due to the move of one industry to Sherwood. Generally, the growth in outside usage is due to the construction of municipal servicing for existing residents who have private wells.5

Overall system pumpage for the test period is forecast to approximate the pumpage level in 1981. However, the CWC indicates that, at present pumping capacity, it is unable to provide for projected growth.

Table 1 shows actual and forecast sales and pumpage data by sales area for the period 1987-1992/93.6

Table 1

Charlottetown Water Commission

Water Sales Forecast

The CWC includes customers in the Hillsborough Development area in the inside-Charlottetown customer group. Other customers not included in the inside-Charlottetown group are categorized by the Utility as outside customers. Outside customers include sales to both individual customers and municipalities.

The general decline in sales volume within the Charlottetown area in the test period is mainly attributed by the CWC to the reduction of 78 million gallons in the metered sales volume at the Perfection Foods dairy processing facility. The CWC projects average sales increases to Sherwood of 29 million gallons and to West Royalty of 16 million gallons in 1992.

The sales variations from 1987 expressed as a percentage change from year to year are shown on Table 2.

Table 2

Charlottetown Water Commission

Water Sales Forecast

(Showing % Change from Previous Year)

The Applicant's customer-base forecast is shown on Table 3.

Table 3

Charlottetown Water Commission

Customer Base Forecast

The forecast used by the CWC in this application has been examined by the Commission and is considered acceptable. The Commission is satisfied with the level of detail applied by the CWC in its forecasting process and believes that the results of the forecast, although largely based on judgment, are reasonable.

The Commission believes that the CWC should have in place a procedure that will allow its staff to carry out, on an annual basis, internal sales forecasting. The magnitude of the increase sought in this application leads the Commission to believe that improvements in this area are needed. In our view, improved internal forecasting would mitigate the possibility of the Applicant having to seek such a substantial increase in the future.

The Commission also believes that the accuracy of the CWC's sales estimates for residential customers could be improved upon through the implementation of a more comprehensive program of meter sampling. While the CWC witnesses suggest that the cost of additional meters would outweigh the benefits obtained from these meters, we were left with the impression that this matter has not been properly investigated. Given the importance of such data to the system, we believe that further efforts should be made in this important area.

The filing requirements that follow are made by the Commission to ensure that the CWC implements improvements in the above areas. These procedures combined with the annual financial budgeting process should better enable the Applicant to plan for changes in its financial position well in advance of a requirement for amendments to its Tariff.

1. The Charlottetown Water Commission shall file with the Commission, by November 30 of each year, a forecast of its water sales and customer base for the ensuing calendar year.

2. The forecast in 1 shall be prepared in a form similar to Tables 1 and 3 herein.

3. This filing requirement is to commence with a filing in November, 1992 and shall remain in effect until otherwise determined by the Commission.

4. The CWC shall develop for the review and approval of the Commission a proposed program for the improved gathering of metered consumption data for residential customers.

5. The proposed program in paragraph 4 together with a program cost estimate shall be filed with the Commission by September 30, 1992.

Commission staff will be available to assist the staff of the Utility on the implementation of these requirements. The Commission is confident the CWC can carry out this procedure without the use of consultants.

2.3 Accounting Matters

2.3.1 Introduction

Since the mid-1970's, the CWC has employed the cash-needs method of accounting. The method differs from utility accounting in the manner in which capital assets are treated. The CWC proposes the continued use of the cash needs method albeit it employs a form of the utility method in the determination of its revenue requirement and the rate base–rate of return method in its cost allocation and rate design model.

The cash needs method used by the CWC divides capital purchases into categories referred to by the CWC as small and large with the former being amortized over periods of up to eight years depending on the estimated life of the purchase. Large capital items are usually acquired with interim financing and eventually financed with 20-year debt instruments thereby spreading the cost of the capital assets over a 20-year period. In addition, in 1987 the CWC adopted a procedure of amortizing the cost of capital items over a 15-year term where such items had been financed with internally generated funds.

The traditional utility method of accounting establishes a rate base upon which a rate of return is awarded. The return component of revenue requirement is intended to recover costs associated with return on capital. Recovery of capital is dealt with through charges for depreciation.

The Charlottetown Water Commission takes the position that its use of the cash needs accounting method is a generally-accepted industry practice. It cites several publications from the American Water Works Association ("AWWA") in support of this position. Moreover, it submits that, regardless of the method required by the Commission, it is entitled to publish its financial results in whatever form it chooses. In the words of CWC Counsel:

CWC currently submits financial information that fully satisfies the requirements of the regulatory legislation. CWC has good reason for developing and maintaining further and other financial information. It has consistently been the position of CWC that the Commission does not have the legislative mandate to determine the contents or methodology of CWC's additional financial records, administration or published financial statements beyond fulfillment of the Commission requirements.7

The CWC does accept, for regulatory purposes, the traditional rate base - rate of return accounting method. It rejects a third method—referred to at the hearing as the modified utility method—an approach that had been in recent use by the PUC. The latter approach differs from the rate base - rate of return approach in two principal areas: a limit is placed on capital expenditures from current revenues and the return component is eliminated.

The accounting issue in this case arose as a result of staff-directed interrogatories. Staff took the position that, since the filings of the CWC relating to accounting did not follow the recent practices of the PUC, the matter required review. As a result of the responses filed by the CWC to these interrogatories, the Commission retained—on recommendation from staff—a chartered accountant to give independent evidence on the issue. Gerard Fitzpatrick was engaged for this purpose and gave evidence at the hearing

The views of Mr. Fitzpatrick and those of the CWC and its accounting advisor, J.M. Mulligan, on the issue of the CWC's accounting practices differ on a number of matters.

The Commission's interest in the area of accounting for public utilities and the need for uniform application of accounting methods is perhaps best described as follows:

Several basic objectives of accounting regulation can be realized under uniform systems of accounts. In the first place, rate regulation requires accurate records of revenues, operating costs, depreciation expenses, and investment in plant and equipment, among others. Here, uniformity is essential to effective commission staff audits, and where applicable, where rate regulation is undertaken on an industry wide basis. Uniformity also is desirable so that public utilities are not subject to different accounting regulation...

[A]ccounting regulation is needed so as to distinguish between expenditures that should be charged to capital and those that should be charged to income. Expenditures that represent investment in capital assets should be charged to fixed asset accounts rather than to operating expense accounts. Similarly, expenditures that represent costs of doing business should be charged to operating expense accounts rather than to capital. If these distinctions are not made, earnings can be inflated by charging operating expenses to capital, or concealed by charging capital to operating expenses. Again, uniformity is essential, for without it the accounting practices of the various companies would differ. One firm might charge all replacements to operating expenses, even if the expenditures were for improved equipment. Another firm might distinguish between an expenditure that represented a replacement in kind and one that represented an improvement, charging the first to operating expenses and the second to capital. Such varied practices would make industry wide comparisons impossible.

...

[A]ccounting regulation is of aid to the commissions and utilities in evaluating the reasonableness of rates. Public utilities provide many different types of services. Unit cost information is essential in controlling price discrimination and in determining the profitability of competitive rates.8

It is the Commission's view that uniform accounts and uniform application of accounting methods are essential to the effective regulation of public utilities in Prince Edward Island. With this in mind, we will focus our attention on the specific areas in contention.

2.3.2 Treatment of Capital Assets—

Capital Recovery and Depreciation

Public utilities are traditionally capital intensive. As has been noted by Bonbright:

Most regulated industries are capital intensive. For instance, utilities often have $3-$4 of assets for every $1 of sales, whereas for manufacturing companies the ratio is $.80 of assets for each $1 of sales.

...

[U]tilities need to maintain excess capacity to meet peak demands and generally to maintain direct connections by wire, pipe, or other means, with their customers. Customers have great difficulty changing suppliers. Suppliers therefore can control use and can prevent reselling, which, taken together with varying elasticities, make price discrimination by them feasible.9

It is therefore apparent that, when comparing a utility with the manufacturing sector, the more capital intensive nature of a public utility combined with a utility's mandated need to maintain excess capacity results in the cost of capital of a public utility having a greater influence on the cost of the service it renders.

This makes relevant the Applicant's method and timing for the expensing of capital assets. Central to this whole issue is the manner in which, from an accounting perspective, capital assets are treated.

The Charlottetown Water Commission prefers the cash needs accounting method for internal and public reporting purposes. It has used and continues to use the rate base—rate of return method for regulatory reporting purposes by transposing its cash needs requirements into the categories deemed appropriate for regulatory purposes. The cash needs accounting method as applied by the CWC includes recurring operating costs, costs of servicing and discharging the debt and costs associated with amortizing the cost of assets for which no debt was incurred.

This Commission and indeed most regulators of public utilities require the use of depreciation as a charge against operations for asset consumption. In describing the value of depreciation to regulators, James E. Suelflow has this to say:

Providing for depreciation oftentimes is termed an accounting procedure as opposed to a cash expenditure. This is essentially true since the transaction does not involve the disposition of funds. Inasmuch as there is no cash outlay involved, the mere accounting entry serves to recognize a proper cost and prevent an improper distribution as dividends to equity holders or a transfer to the utility's retained earnings account. Regulators are vitally concerned with utility depreciation practices since control of these will be reflected in the rates charged to the consumer...10

The Water and Sewerage Act gives the Commission some guidance in its consideration of this matter. Some relevant sections of the Act that relate to accounting or accounting-related matters follow:

11.(1) Every public utility shall carry a proper and adequate depreciation account when the Commission, after investigation, shall determine that the depreciation account can be reasonably required.

(2) The Commission shall ascertain and determine what are proper and adequate rates of depreciation for the several classes of property or material of each public utility.

12. The Commission may prescribe the form of books, accounts, papers and records required to be kept by a public utility, and every public utility is required to keep and render its books, accounts, records and papers accurately and faithfully in a manner and form prescribed by the Commission and to comply with all directions of the Commission relating to the books, accounts, papers and records.

13. The Commission may cause to be prepared suitable blank forms and shall, where necessary, furnish the forms to each public utility, which shall make thereon such reports to the Commission as it may require.

14. The Commission may direct that a public utility shall make certain provisions for the amortization of any sums allowed for organization expenses and expenses of valuation, and may direct that the sum required annually for the amortization shall be charged as an operating expense.

The Commission interprets these sections as giving it broad authority over the system of accounts and accounting method or methods used by public utilities.

The Charlottetown Water Commission's accounting procedures as they relate to the treatment of capital assets is described in the following evidence of Mr. Mulligan:

The records of the Utility are kept on a cash needs basis as described in the AWWA Manual of Supply Practices (M1. Section 1). This basis has been used consistently for 16 years, since 1975, and comparative information is also available for 1974.

...

The cash needs system used for accounting purposes by the Charlottetown Water Commission has its basis in cash budgeting which is done annually and approved by the Commissioners who are elected by the rate payers to run the utility.

This system is not to be confused with the cash basis used by farmers under the Income Tax Act or the cash basis system described to me by Mike Loudon which is predominant in Ontario utilities. These systems include in expenditures the cost of assets acquired or debt retired in the year of payment.

The main difference from the above-mentioned cash basis systems is that:

1. The cash needs system adopted by CWC incorporates the use of a depreciation method which retires or writes off fixed assets by retirements out of revenue and contributions in the form of grants or payments by owners for services being installed. Retirements are in effect a replacement for % or rates of depreciation.

2. In all other respects, full accrual accounting methods are used.

The system is founded on the fund accounting system used by municipalities for many years. The amount of retirements included in the expenditures each year is based on the amount of small capital assets acquired and the amount of debt repayments required on long-term debt, as well, when the long-term assets are financed by bank loans and no repayment terms are negotiated, the Commissioners may decide to retire some of the debt (in order to reflect in operations the cost of the assets being used). The length or the term of the debt is decided by the [CWC] Commissioners when they issue the debt instrument. The decision is usually made based on quotations from financial houses who quote interest rates and the repayment terms available. Under the system, reserved [sic] funds could be established if the [CWC] Commissioners decided reserves were needed.

The financing decisions made by the [CWC] Commissioners are on the basis of keeping the utility in good financial condition and, as much as possible, keep the rates as low as is practical and in keeping with good financial management.

...

Depreciation is not included in the calculation of funds required on a cash needs basis but is used on a net basis to determine the return on rate base on a utility basis.11

The above description of the accounting practices of the CWC indicates that a large measure of discretion is left with the members of the CWC over the treatment of capital assets both in the initial classification of the asset and the manner in which the asset is expensed or charged against income. It is evident from the testimony of its witnesses that it wishes to retain this discretion and, although there is no evidence of abuse of this discretion by the present members of the CWC, we regard the potential for improper use of uncontrolled discretion to be a significant drawback in the cash needs accounting method.

Industry literature seems to support the use of both cash basis accounting and utility basis accounting. Cash basis accounting as described by the AWWA considers revenue requirement components to include operation and maintenance expense, debt-service requirements and capital expenditures not debt financed. The latter component—capital expenditures not debt financed—is described by the AWWA as follows:

Capital expenditures are generally classified into three broad categories: replacement of existing facilities, normal extensions and improvements and major capital improvements and replacements. It is a generally accepted practice to finance normal replacements and extensions and improvements from current revenue, but some utilities also use current revenue to finance a portion of major capital improvements and replacements. However, most major projects are financed from serially funded debt because the repayment of the debt over a number of years distributes the capital costs, to some extent, over the useful life of the facility. This debt-financing approach results in better matching of the customers' charges from year to year with the use of the facilities. (i.e. existing customers will not be paying 100 percent of the initial cost of facilities to be used by future customers).12

The utility basis of accounting is described by the AWWA this way:

The utility basis of determining revenue requirements is mandated for all investor-owned water utilities and for most publicly owned (municipal) systems under the jurisdiction of state commissions or other regulatory bodies.

...

The use of the utility basis can reduce controversy since it generally results in more stable rates because they are not so immediately affected by the level of system capital expenditures as are rates under the cash basis.13

However, in its continuing description of the utility basis, the AWWA goes on to state:

For a publicly owned utility, the total level of annual revenue required is the same under either the cash or the utility basis. The operation-and-maintenance expense component of total revenue requirements is usually identical under both methods. The annual cash requirement for capital-related costs under the utility basis of revenue-requirement determination, consists of the two components of depreciation expense and return on rate base.14

This description by the AWWA has been the cause of much of the debate at the hearing. When originally reviewed by the Commission, we had the impression that, since the two methods were, according to the AWWA, supposed to generate the same results, the arguments we were hearing on the issue were largely redundant. However, it has become apparent to the Commission that, when the purpose of the exercise is to critically analyze the components of revenue requirement, the statement of the AWWA seems equivocal. For example, in an accounting publication, the AWWA makes the following statement:

Ordinarily, the revenue requirements as determined by the two different approaches would differ.15

In the same publication, the AWWA has this to say:

In the case of investor-owned water utilities and municipally-owned water utilities subject to rate regulation by state public service commissions, revenue requirements generally are established by applying the traditional public utility approach: the determination of gross revenues sufficient to permit a given return on a defined rate base. The NCGA16 strongly recommends that municipally-owned utilities use the same approaches as those in private industry, including charging depreciation. Therefore...the traditional public utility approach also is recommended for use by municipally-owned water utilities not subject to regulation by public service commissions, rather than the 'cash needs' approach. The traditional public utility approach is consistent with the accrual basis of accounting and with depreciation accounting, whereas 'cash needs' is not.17

In his evidence on this topic, Mr. Fitzpatrick presents the following view:

In keeping with the principle that present customers should only pay for the cost of operations and the cost of facilities consumed in providing service to them, one could look at the following comments:

Depreciation is a real part of the cost of operating a utility, whether publicly or privately owned. Depreciation is the loss in value of facilities, not restored by current maintenance, that occurs in the property due to wear and tear, decay, inadequacy, and obsolescence. The annual depreciation-expense component of revenue requirements provides for the recovery of the utility's capital investment over the anticipated useful life of the depreciable assets. It is therefore proper that this expense be borne by the customers benefiting from the use of these assets during the period. The proper level of depreciation expense to be included in the total revenue requirement should be based on the cost of the depreciable plant in service during the period for which rates are being established. The funds resulting from the inclusion of depreciation expense in the annual revenue requirements are the property of the utility and are available for use as a source of capital for replacement, improvement or expansion of its system or for repayment of debt. (AWWA M1, Page 3 of 3).

This comment leads one to believe that assets consumed are charged against customers consuming them. The following comment on cash basis accounting does not leave one with the same secure feeling.

Most major capital projects are financed from serially funded debt because the repayment of the debt over a number of years distributes the capital costs, to some extent, over the useful life of the facility. (AWWA M1, Page 2 of 3)

...

On a theoretical basis, if a consumer is just to pay for the cost of an operation, the operation should operate at a break-even each year. The use of retained earnings...to finance the capital expenditure activities of a municipally-owned water utility results in a cost to water customers in the sense that charges for water service are higher than is necessary to cover current costs of providing the service by the amount used to finance capital expenditures from retained earnings.18

The Commission believes that the CWC's particular application of the cash needs accounting method implicitly recognizes one of its principal difficulties: the matching of asset consumption with asset cost. The CWC's recent adoption of a 15-year amortization period for assets purchased without debt financing is, in our view, an attempt on the part of the CWC to adjust for this.

Mr. Mulligan gave evidence for the CWC that he believed the cash needs system was superior to the utility method of accounting because

1. it provided better information by which the utility could judge its cash flow requirements; and

2. it was easier for the CWC Commissioners to understand.

The length of time required during the hearing for explanations of the statements prepared on the cash needs basis has led the Commission to question the suggestion that these statements are inherently easier for the CWC Commissioners to understand. Our conclusion is that they can only be "easier to understand" because they have been used for many years. A similar ease of understanding would develop with statements prepared on a utility basis after they were explained and in use for a while.

For the many reasons already referred to, the Commission has decided that the CWC must adopt the utility basis for its reporting to the Commission. Although we would prefer that the CWC prepare all of its financial statements in this way, we are not prepared to make an order to this effect at this time. Because of this, we find it unnecessary to make a decision on the issue of our authority in this area. However, having reviewed the legislative authority, we point out that it is very broadly worded and seems to indicate authority over all records and reports.

As indicated previously, the Commission found the cash needs accounting statements quite difficult to understand and would therefore request the CWC Commissioners to review this issue to determine whether they can use the utility method for all purposes.

6. Financial statements and applications for Tariff amendments hereinafter filed with the Commission by the CWC and the system of accounts used by the CWC shall comply, with the necessary changes, with the NARUC19 Uniform System of Accounts for Class A Water Utilities and shall be presented on a utility basis.

7. These statements shall be audited and shall contain a statement from the auditor that they comply with the said Uniform System of Accounts.

8. The requirements in paragraphs 6 and 7 apply to financial statements prepared for the year ending December 31, 1992 and thereafter until otherwise ordered by the Commission.

The application of the above requirements necessitates a Commission determination on appropriate rates of depreciation. In addition, the Commission is asked by the CWC to vary the standing practice of the PUC of requiring the application of depreciation on a gross-asset basis.

Table 4 shows the Applicant's present and proposed depreciation rates and depreciation expense for water system plant on a net-cost basis.

Table 4

Charlottetown Water Commission

Depreciation Rates - Water

(December 31, 1990 Data)

Table 5 shows the same data for the CWC's sewer system.

Table 5

Charlottetown Water Commission

Depreciation Rates - Sewer

(December 31, 1990 Data)

The Applicant's current rates of depreciation were established some twelve years ago. In its description of the approach used in determining the proposed depreciation rates, the CWC stated:

The rates used in the test year of 3.51% of water assets and 2.31% of sewer assets were established by comparing the individual rates used to establish the composite rates in 1979 by the Public Utilities Commission with the rates regulated by the N.S. Public Utilities Commission [sic] and selecting the rates considered most appropriate and applying the individual rates to the assets now on hand in the various classifications as at December 31, 1990.20

The Commission agrees that the current rates in effect for the CWC are in need of review. However, we are unable to accept a comparison with Nova Scotia rates as sufficient grounds for a change. In our view, the matter requires further study.

The Commission is prepared to sponsor a study of the depreciation rates in use by the CWC and other utilities in the Province to ensure that any new rates are, within the Prince Edward Island context, proper and adequate. The CWC will be consulted during the study-phase and, if necessary, the Commission review-phase of this project prior to the implementation of any study recommendation.

In the meantime,

9. The new rates of depreciation proposed by the CWC in this application are, at this time, denied.

10. Pending the outcome of a Commission-sponsored depreciation study, the CWC shall use classified or individual rates of depreciation.

11. For the purposes of paragraph 10, the classified or individual "1979" depreciation rates are to be used.

The Applicant's proposal to apply depreciation on a net-asset basis is supported by both Mr. Mulligan and Mr. Fitzpatrick. The Commission agrees that this practice better reflects the cost to the consumer.

12. The proposal of the CWC to calculate depreciation expense on a net-asset basis is approved.

We turn our attention now to the matter of rate base and rate of return.

2.4 Rate of Return

The CWC seeks a rate of return on rate base of 15.38%. This equates to a dollar return of approximately $729,000 on a combined net-asset rate base of $4,748,776. The calculation of the return requested by the CWC is shown in Table 6.

Table 6

Charlottetown Water Commission

Calculation of Rate of Return

The CWC's calculation of the components of revenue requirement calculated on a utility basis is shown on Table 7.

Table 7

Charlottetown Water Commission

Revenue Required from Rates

Utility Basis

The return component in this calculation is made up of debt interest ($245,595), other required operating revenue ($86,412), and shortfall recovery ($108,000). On a component-cost basis, the return of $440,007 on a rate base of $4,748,776 equals a rate of return of 9.27%—less than the return requested in the application.

The rate base–rate of return concept of regulation is widely used in the industry, particularly in the United States. In Canada, the practice is less prevalent although the concept of a fair return on utility capitalization is universally accepted.

In Prince Edward Island, the use of rate base–rate of return regulation has traditionally been limited to electric power regulation. However, this form of regulation had been used by the PUC in a limited manner in the regulation of municipal utilities, including the Charlottetown Water Commission.

Rate base–rate of return regulation as applied by most regulatory agencies involves an analysis of the specific costs associated with return on capital. Usually included in this analysis is a review and determination of the appropriateness of the capital structure of the utility.

In a privately-owned utility, the rate of return includes interest costs associated with debt as well as a return on equity. In publicly-owned utilities such as the Applicant, the return includes costs associated with debt. It may, however, include some form of return or net income allowance.

The concept of an equity return or net income allowance for publicly-owned utilities has, in recent years, gained support in many areas of the country. In fact, in a 1988 decision of the PUC, the following comments are found:

The Town now proposes that it be permitted to recover an amount from its rural customers as a coverage on its debt interest. According to Mr. Richardson:

The Town of Summerside puts its taxpayers on the line as guarantors when it borrows money for the utility. Also, the magnitude of the total operation of the Town - General, Electric, Water, Sewer and Pollution Utilities - enables the Town to borrow at lower rates than the electric utility could get on a stand-alone basis. Some payment for this guarantee and economy-of-scale effect on interest rates makes common sense, in my opinion, and interest coverage is a logical way to assess the customers for these benefits.

It is, we believe, well established that a corporation, whether public or private, ought to recover, as part of its revenue requirement, a margin over its actual cost of service to maintain or achieve a sound financial position. Such a margin must, however, be based on sound financial principles as opposed to purely arbitrary determination.

In the case of public corporations such as the Applicant, the Commission considers that normal financial standards should apply in the determination of the revenue requirement. One such standard, the interest coverage test, is advanced herein. Regrettably, however, a full discussion of the merits of applying normal standards has not formed part of this proceeding. The Town may wish to adduce further evidence on this topic at a future rate hearing.

For the purpose of this decision, we will accept the 1.1 times interest coverage proposed by the Town.21

In seeking the return requested herein, the CWC submits that the return is needed to maintain the Utility in good financial condition. The Applicant describes this need this way:

The term 'good financial condition' in the context of the [CWC] is one which enables the utility to:

(a) keep rates as low as possible while at the same time providing top level service;

(b) maintain a relationship with the debt financing markets which enables it to borrow funds at favorable rates comparable to other local governments;

(c) maintains a financial condition which allows the Commission to pay its obligation on a timely and appropriate manner without undue stress;

(d) maintain an adequate pension plan for its employees.22

As noted in Table 7, the components of return requested by the CWC under the rate base–rate of return method include:

· Debt Interest in the amount of $245,595;

· Shortfall Recovery in the amount of $108,000; and

· Other Required Operating Income of $86,412.

The debt interest expense is properly included as an item for recovery through rates. The proposed amount is allowed.

13. The debt interest expense of $245,595 proposed by the Applicant is allowed.

The shortfall recovery expense is described by the CWC as a budgeted addition to the revenue requirement of $108,000 annually over the next four years to recover the projected accumulated shortfall or loss in the CWC's level of retained earnings. The CWC submits that it requires a level of retained earnings totaling $432,297 for working capital. According to the CWC:

The shortfall of $108,000 in the years 1992, 1993, 1994 and 1995 is as calculated on page 64 [of Exhibit A-1]. The 'Water Utility Capital Financing', A.W.W.A. M29, 1988, manual on page 55 defines 'working capital' as:

cash, materials, supplies, and other similar current assets necessary in the operation of the enterprise. It is usually measured by the excess current assets over the current liabilities or sometimes as a portion of the annual O&M expense levels.

The A.W.W.A. M35 Manual, Revenue Requirements states on page 33:

The primary elements of working capital include materials and supplies and cash-working capital. Other elements may include prepayments, unamortized balance of non-annual (O&M) expenses and minimum bank balance.

The allowance for working capital in rate base permits the utility to earn a return on the investment required to finance operating costs in advance of the receipt of revenue. Normally, there is a lag between the payment of costs and the receipt of revenues. Sometimes the receipt of revenue leads the expenditure. A detailed 'lead lag' study can be performed to determine the weighted average period of time between cost and revenue. The working capital requirement is the average daily amount of the costs x the average time period determined from the lead lag study. In the absence of a lead lag study, the 45 day rule is frequently used when monthly billing is practiced. The average daily amount of cost is multiplied by 45 to determine the working capital allowance to reflect the billing period plus a lag in payment.

Since C.W.C. uses a bi-monthly and quarterly billing period, we have adjusted the 45 day rule to three months, or 1/4 of our annual revenue requirement (i.e. our expenditures). The 90 days equates to the 45 day rule (i.e. 1 1/2 times 30 days is 45, 1 1/2 times 60 days is 90 days.23

It will be noted that the Applicant does not propose the addition of necessary working capital to the rate base. Rather, it proposes the addition to revenue requirement. In other words, it seeks the advance of money from the ratepayers to fund rather than finance working capital requirements.

Working capital is a legitimate cost of doing business. In traditional rate base–rate of return regulation, the requirement or regulatory allowance for working capital is, as the AWWA suggests, determined by the application of a lead lag study or an established rule. The allowance is added to rate base. The return on rate base award of the regulator recovers, among other things, a utility's cost of financing working capital requirements. It does not, as the CWC proposes, allow the utility to receive an advance from the customer to wholly fund the requirement. The matter of an appropriate working capital allowance is dealt with later in these reasons.

In 1987, the Indiana Public Service Commission was faced with a similar request for recovery of a past deficit. The Indiana Commission categorized this as retroactive rate making and stated:

If a utility has taken all reasonable steps to reduce its operating expenses and thereafter finds itself unable to generate its statutory revenue requirements, prudent business practice would indicate that it is time to file for the appropriate form of rate relief. Through its own action, this Commission is familiar with the onerous responsibility of making unpopular decisions. Nevertheless, the burden of pursuing appropriate rate relief when needed is part of the managerial decision making responsibility which falls upon the shoulders of governing bodies of municipalities. On the other hand, if a municipal utility, in full recognition of its inability to meet its cash revenue requirements, decides to transfer money from its municipal fund and/or allow its deficits to grow, then that is a decision for which the municipality must accept responsibility. Meeting the direct and clearly foreseeable direct financial consequences of such action is not a burden which this Commission will transfer to rate payers through retroactive rate making or through inappropriate use of cash revenue from working capital... This Commission cannot protect municipal utilities from the effects of past omissions from burdening the rate payers with the financial consequences of those omissions. The Commission finds the Petitioner should not be allowed additional revenue for cash working capital.24

The Commission agrees with these statements. For the reasons given, the Commission cannot accept the Applicant's request for the shortfall recovery of $108,000 per year over the next four years.

14. The 'Shortfall Recovery Expense' of $108,000 proposed by the Applicant is disallowed.

As noted above, the concept of an equity return or net income allowance for publicly-owned utilities is gaining general support among Canadian regulators. Whether this element of expense is considered a return item under traditional rate base–rate of return regulation or a net income allowance to be retained by a utility is immaterial. The issue of financial integrity and the number of dollars needed to ensure such integrity is.

As in the case of Re Town of Summerside Electric Department, the Commission accepts the principle that a publicly-owned utility should be permitted to recover, as part of its revenue requirement, a margin over its actual cost of service to maintain its financial integrity. Unfortunately, there is little guidance to be found on this issue through Canadian material relating directly to water utilities. Indeed, even cases relating to the United States are difficult to rationalize. Overall, however, the principle of a return or allowance of some type is supported.

In considering the application of normal financial standards or theory in determining an appropriate return or allowance for a municipally- or other publicly-owned utility, the Commission had to rely on case material at its disposal. Considerable time was spent by the Commission researching this matter subsequent to the hearing.25

In the absence of specific submissions by the CWC on this issue, the Commission believes that the financial integrity of the Applicant is properly measured through recognition of a utility's debt interest coverage ratio. The Other Required Operating Income of $86,412 proposed by the CWC when viewed as a coverage on debt interest renders the following debt interest coverage ratio for the Applicant.

Table 8

A debt interest coverage ratio in the range of 1.30 to 1.35 times is, in the Commission's view, an acceptable coverage allowance for a relatively small municipal water utility. Such a coverage recognizes the inherent risk assumed by the City of Charlottetown in its effective guarantee of the debt of the Utility. Moreover, it will permit the Applicant to improve, over time, the equity component of its capital structure which in the last two years has deteriorated sharply.

15. The Commission hereby establishes a target debt interest coverage ratio for the Charlottetown Water Commission in the range of 1.30 to 1.35.

16. This target ratio is be reviewed from time to time and will be adjusted by the Commission where deemed necessary.

In reaching these findings, the Commission has made no determination on an appropriate capital structure for the CWC and, in particular, the level of equity that should, over time, be attained by the Utility. The CWC should adduce evidence on this topic when it next appears before the Commission.

For utility planning purposes, the Commission believes the ongoing use by the Applicant of a debt interest ratio as a target for net income purposes will facilitate the planning process. And it will be used by the Commission for that purpose. However, in view of the Applicant's stated desire to be permitted a rate of return on rate base, the allowance based on the target debt interest coverage ratio can be converted to a return on rate base.

Table 9 shows the conversion.

Table 9

The Commission will add to the rate base and rate of return an amount for necessary working capital. Because the CWC's billing process includes both advanced billing for flat rate customers as well as billings for actual metered consumption, we are not convinced that the 90-day working capital proposal of the Applicant is necessarily correct. For regulatory purposes, we will employ a working capital allowance of $250,000 in rate base and the interest costs—at a rate of 10% thereon—in the return component. This approximates the 1/8th or 45-day rule which is widely used. When it next appears before the Commission, the CWC should, if it intends to continue to utilize the rate base–rate of return approach, include a lead lag study in support of its working capital proposal.

Table 10 shows the rate base–rate of return adjustment.

Table 10

In the result,

17. The allowable rate of return on rate base for the Charlottetown Water Commission is established at 7.07% 2.5 Operating Expenses

The Applicant's test year level of operating expenses is $2,013,698. This is the average of forecast expenditures totaling $1,973,300 in 1992 and $2,054,095 in 1993.

Table 11 shows the Applicant's operating expenses by account function from 1988 to the 1992-1993 test year. The figures for 1988 - 1990 are actuals.

Table 11

The evidence of CWC witness MacLeod and a review of the detailed sub-accounts of the applicant as shown on pages 67-1 to 67-7 of Exhibit A-1 reveal the general use of a 6% and 5% across-the-board budgeting process for the years 1992 and 1993. Although Mr. MacLeod commented that the budgeting process used by the CWC is zero-based, it is apparent that, in general, a simple incremental budgeting process is used.

In our overall review of this case, it became apparent to the Commission that, over the last few years, the CWC has made great progress in the area of system operations through such things as computerized automation. The operating data supplied at the hearing and the description by Mr. Clark of the advances the CWC has made in this area are evidence of the attention that has been paid to Utility operations.

The CWC, however, continues to use a manual budgeting process. In the Commission's view, the CWC should make available to its Secretary-Treasurer and his staff microcomputer facilities and training in the use of spreadsheets. In our view, the overall benefits that will accrue to the CWC and its customers of computerizing this area will far outweigh the costs.

The specifics of the 1992-1993 operating budget were reviewed in some detail at the hearing and have been fully considered by the Commission. As the Commission views this hearing as a first in what will be a more regular and more frequent review process, we have decided in these reasons to discuss the forecast in general rather than specific terms in the hope that the Applicant will better understand the regulatory process. When it next appears before the Commission, the CWC's forecast will be subject to more detailed analyses and comment.

To this end,

18. All future rate filings of the Charlottetown Water Commission shall include a detailed expense forecast with written evidence describing the budgeting process and the specifics of each budget item.

An area of the Applicant's forecast that causes us particular concern relates to increases in salaries and wages. As we understand it, the Utility has budgeted increases in these areas of approximately 6% in 1992 and 5% in 1993.

The Commission understands from the evidence that these proposed increases are nothing more than an extension of the across-the-board incremental budgeting process rather than a true reflection of the increases that will be given. In light of present economic conditions as well as recent wage settlements in the public sector, we view the six-and-five proposal as excessive and something that is not reasonably passed along to the consumer.

For budgetary purposes, we will limit these increases to two percent in each of the two years. Although this has a very minor impact on the Utility's salary and wage-related expenses—approximately $20,000 in each of the years—we are unable to sanction the proposal. The allowed expenses are reduced accordingly.

The other proposed expenses are, however, allowed, notwithstanding our belief that they may be marginally overstated. As noted above, future reviews of the CWC's expenses will be more critically reviewed to ensure that they are reasonable in relation to the services provided.

Finally, the Commission notes the proposal of the CWC to proceed in 1992 with its plans to develop a new well field. Although the CWC in this application does not seek regulatory approval of these plans, we want it clearly understood that the project will require regulatory approval prior to its commencement. A project of this magnitude must not proceed without a full public discussion of its overall impact on the consumer.

Based on the above discussion,

19. Operating, maintenance and administration expenses in the test period totaling $1,993,698 are allowed.

2.6 Overall Revenue

Requirement

The Utility's overall revenue requirement as approved by the Commission is shown on Table 12.

Table 12

Part Three

Proposed Rates

3.1 Introduction

This chapter concerns itself with the Applicant's rate proposals. The Commission's interest in this area is twofold:

· to ensure that the proposals are, in all respects, reasonable and non-discriminatory; and

· to ensure that the proposals generate the revenue requirement.

The reasonableness of rates is often measured against the cost of serving individual customers or customer classifications. Essentially, rates should fairly represent the cost of service.

In practice, the determination of rates is a process of allocation. As in all cost allocation and rate design procedures, the process requires the application of a large degree of judgment.

In what follows, the Commission will briefly review the method used by the CWC in determining its rate proposals followed by a discussion of the specific rates proposed herein.

3.2 Cost Allocation

The Charlottetown Water Commission employs the base-extra capacity method of cost allocation and rate design. The method was used by the CWC in its 1980 rate application and is widely used in Canada and the United States.

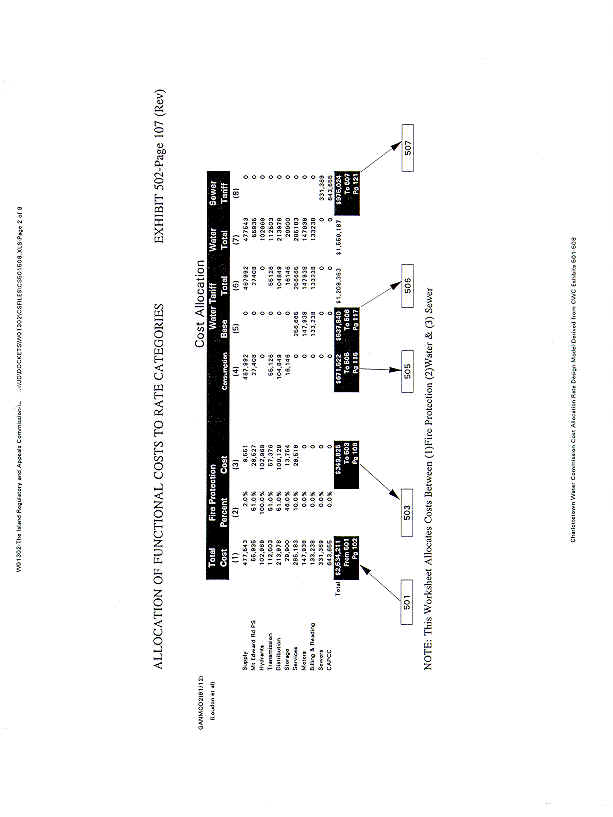

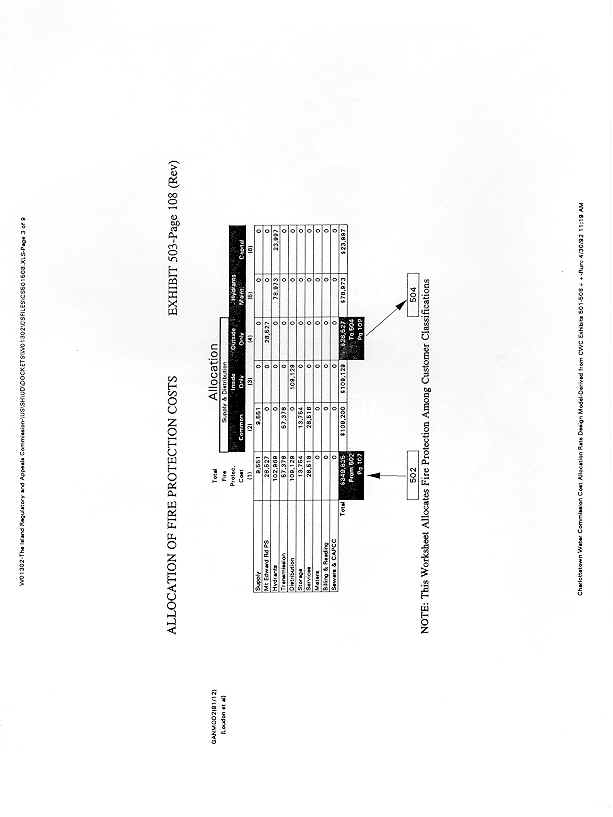

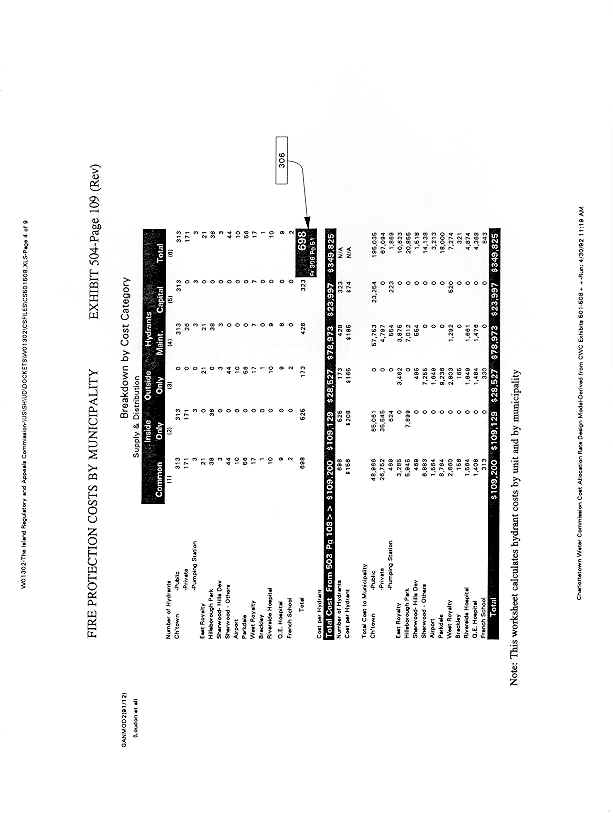

The base-extra capacity method allocates costs that are determined on a rate base–rate of return method of calculating revenue requirement. Costs associated with operations, depreciation and return on rate base are functionalized, or allocated to service functions. Thereafter, the functionalized costs are allocated to service categories, such as fire protection, water service and sewer service. Costs within each service category are distributed to base or demand and volume or consumption tariffs.

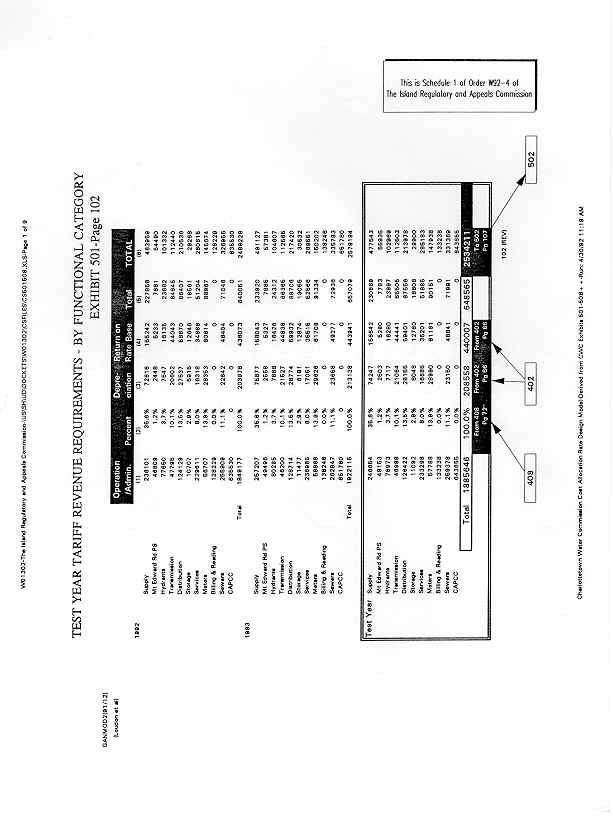

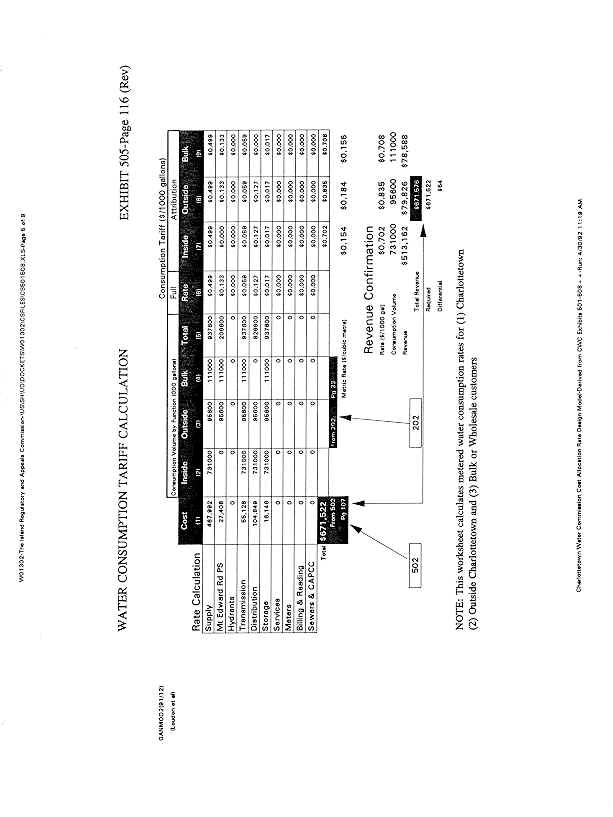

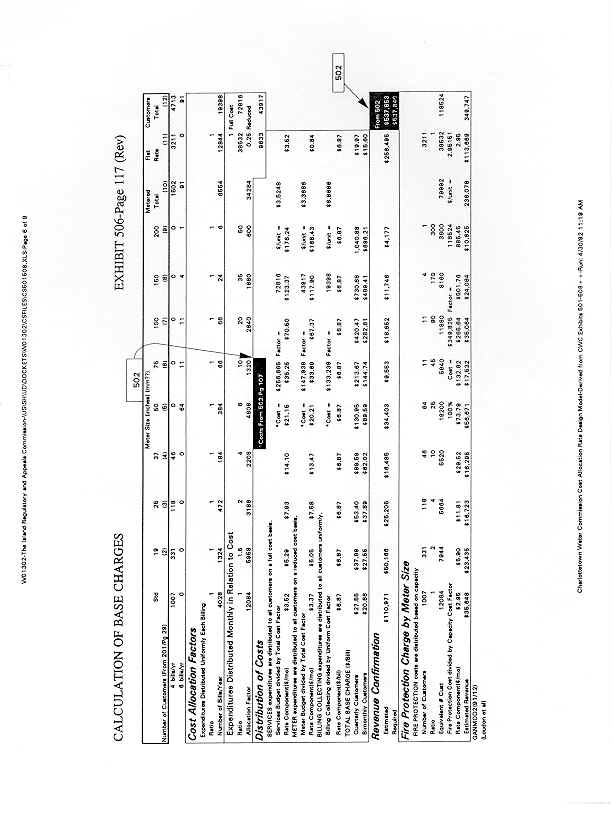

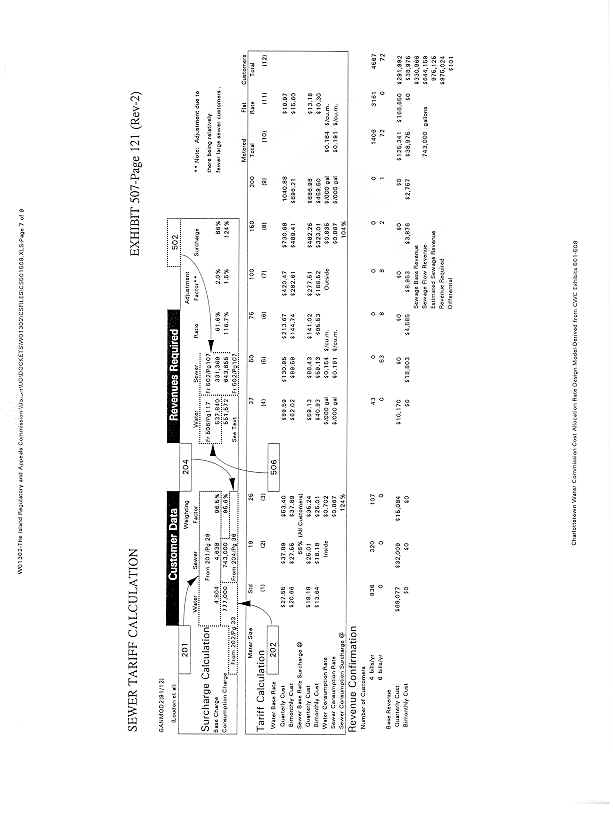

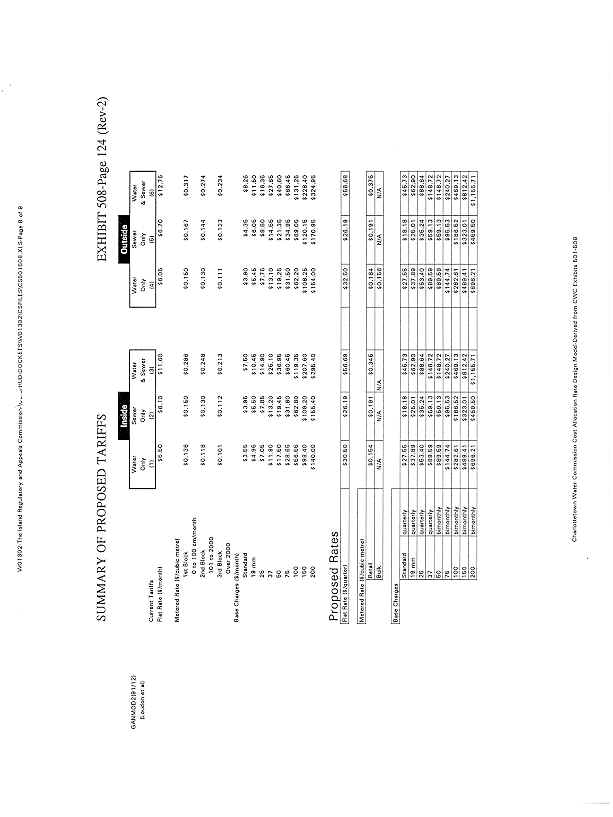

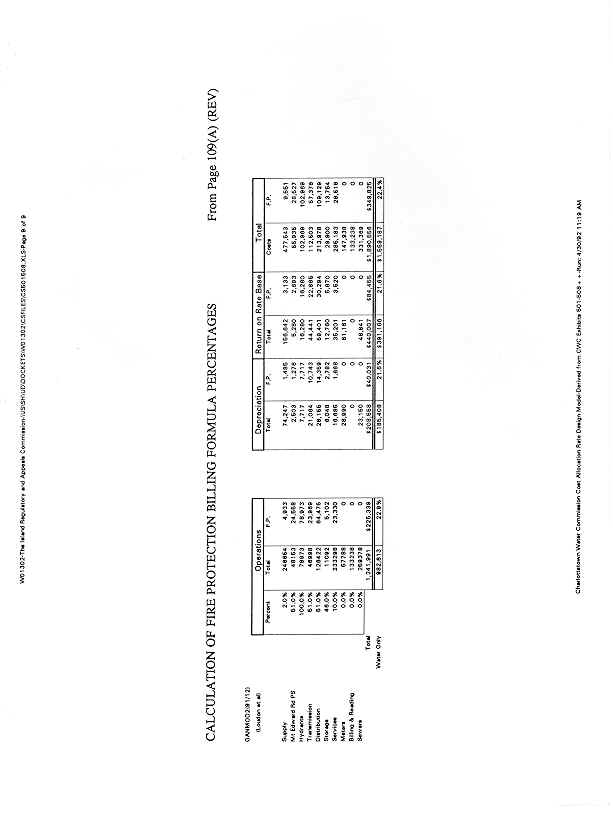

For the purposes of these reasons, the Commission considers it unnecessary to describe the detailed process used by the Applicant in the determination of the Tariff proposals before us. However, for the assistance of the reader, the cost allocation and rate design model employed by the CWC in this application is contained in Schedule 1 of this Order. References in the Schedule to Exhibits refer to documents contained in Case Exhibit A-1.

Having considered the cost allocation model advanced herein, the Commission will accept its continued use by the CWC. In our view, the model apportions costs in a fair and reasonable manner.

20. The Applicant's use of the base-extra capacity method of cost allocation is accepted.

3.3 Rate Design

The overall approach to the Tariff proposals of the CWC in this application are summarized below:

· A two-part Tariff with a basic charge and consumption charge for metered customers and a flat rate for residential customers is maintained;

· A fire protection charge to be levied to the municipality is maintained; however, a proposal is advanced to directly charge customers in the City of Charlottetown for unmetered fire lines;

· The declining block rate structure is consolidated into a single block;

· The former minimum bill for the Charlottetown Airport that was modified by the PUC is eliminated;

· The rates for outside customers are recalculated following cost of service principles; and

· A bulk or wholesale rate is proposed.

With the following exception, the Commission is satisfied with the overall rate design proposals of the Applicant. We are particularly pleased with the bulk or wholesale rate proposal as we consider it a better reflection of the cost of providing water services to another utility for resale.

The proposal of the Applicant to directly charge customers in the City of Charlotteown for unmetered fire lines26 is opposed by the Association of Licensed Community Care Facilities. According to Joe McQuaid, the Association's President:

Community care facilities are required by law to install automatic sprinkler systems for the fire prevention of accommodations for senior citizens. Operators of community care facilities fulfilled this requirement at a considerable expense. For example, a facility housing 15 residents would incur an installation cost of approximately $9,000 and the Charlottetown Water Commission would assess an advance payment of close to $3,000 for service connection costs. Nevertheless, a sprinkler system is a highly efficient fire prevention measure taken by the facilities to protect the lifes [sic] of senior citizens

It is the Association's opinion that the City of Charlottetown and the Charlottetown Water Commission are unfair in attempting to charge a rate on the ownership of a sprinkler system. As members of this community, we have taken additional steps in fire prevention than the average citizen in Charlottetown. Instead of being commended for this action, we are charges an extremely high fee.

Consider this scenario: If similar fires were to start in two homes of the same shape, size, and structure, and one home as oppose [sic] to the other, has a sprinkler system; it is highly probable that the home with the sprinkler system would have extinguished the fire with less water than the home without the sprinkler system. Furthermore, the sprinkler system would require less time and effort from the fire department than the fire fighting to extinguish the fire at the home without the sprinkler system. Thus the system saves not only the lifes [sic] of the inhabitants and the property, but saves the city of Charlottetown's Fire Department and Water Department time, money, and water.

...

The Charlottetown Water Commission's attempt to charge a fee for a sprinkler system is a deterrent to fire prevention. The proposed rate is unfair punishment towards a sprinkler system owner, while a property owner without a sprinkler system receives fire protection subsidized by the proposed fee.27

The CWC's proposal stems from a request made on May 17, 1991 from the City of Charlottetown to the CWC. The City's request noted, in part, as follows:

The City of Charlottetown, during budget discussions in March of 1991, determined that they would no longer as a City Corporation, pay the basic fee for water supply to private buildings equipped with sprinklers.28

The City's comment that it will no longer pay cannot direct this Commission's decision-making. Whether the proposal is reasonable to the CWC and its customers is the deciding factor.

The Commission is of the view that the proposal would result in an undue level of confusion. Moreover, the question of whether a sprinkler system or private fire hydrant benefits the individual customer more than the municipality as a whole is difficult to answer. While one could argue that private unmetered fire lines do benefit the individual customer, there is little doubt that the municipality benefits as well. Simply stated, we see no benefit to the CWC, its customers or the community in changing the status quo.

21. The application to directly charge customers with unmetered fire lines is dismissed.

22. Except as provided in paragraph 21, all other rate design proposals of the CWC are approved.

3.4 Other Matters

During the course of preparing these reasons, the Commission reviewed the statutes governing the operation of the Charlottetown Water Commission. As a regulator, the Commission has an overall responsibility to ensure that the Utility is operating properly and within the law.

For the most part, the apparent discrepancies noted to Counsel for the CWC have been satisfactorily explained. The Commission is not seeking to clear up all matters but rather to ensure that the Utility is aware of potential problems and has taken action where necessary.

The areas where concerns remain are with Sections 16 and 46 of the Charlottetown Waterworks Act and Section 10 of the Charlottetown Sewerage Act. While in many instances we accept that the Water and Sewerage Act supercedes the provisions of these other pieces of legislation, since they were not repealed their provisions will have legal effect unless in conflict with newer legislation. The explanations provided on these points do not indicate that their specific content has been dealt with. These sections appear clear. The CWC must comply with the statutory requirements or have its legislation amended no later than its next hearing.

Finally, on another matter, the Commission is not prepared to again allow an extended period of time to elapse before a review is conducted into the rates and charges of the CWC. Although we don't anticipate that the following requirement will necessarily result in a formal rate case, we believe that, in the long term, the requirement will lower costs as the CWC develops the capacity to produce more information internally.

23. The CWC shall file with the Commission, on a triennial basis, detailed financial and rate information.

24. Details of the form and content of the filings to be made under paragraph 23 will be provided by the Commission to the CWC at a later date.

25. The first filing under paragraph 23 shall be submitted to the Commission by July 31, 1994.

3.5 Disposition

The findings contained in these reasons will necessitate the recalculation of the Applicant's Tariff proposals and the re-submission of the same to the Commission for final approval.

26. The CWC shall forthwith prepare and file with the Commission for review and final approval a Tariff that reflects the findings and conclusions contained in these reasons.

27. The Tariff filed under paragraph 26 shall bear an effective date of April 15, 1992 and shall, on the final approval of the Commission, be effective for bills issued on and after April 15, 1992.

28. Filings made under paragraphs 26 and 27 shall be in written and electronic form and shall contain revenue confirmation calculations and a statement that the filings comply in all respects with the findings and conclusions of the Commission.

Provided the above filings comply in all respects with the findings of the Commission, a final Order of the Commission may be expected within seven days of receipt of the filings.

An Order will therefore issue.

Order

WHEREAS the Commissioners of Sewers and Water Supply (the "Charlottetown Water Commission", the "CWC", "Applicant" or "Utility"), by application dated July 22, 1991, applied to the The Island Regulatory and Appeals Commission ("Commission") for approval of proposed rates and charges for the supplying of water and sewerage disposal services;

AND WHEREAS the Commission heard the application at public hearings conducted in Charlottetown on October 8, 1991 and December 3, 9, 10, 11, 12, 13, and 16, 1991 after due public notice;

AND WHEREAS the Commission has issued its findings in this matter in accordance with the Reasons for Order issued with this Order;

NOW THEREFORE, pursuant to the Island Regulatory and Appeals Commission Act and the Water and Sewerage Act

IT IS ORDERED THAT

1. The Charlottetown Water Commission shall file with the Commission, by November 30 of each year, a forecast of its water sales and customer base for the ensuing calendar year;

2. The forecast in 1 shall be prepared in a form similar to Tables 1 and 3 herein;

3. This filing requirement is to commence with a filing in November, 1992 and shall remain in effect until otherwise determined by the Commission;

4. The CWC shall develop for the review and approval of the Commission a proposed program for the improved gathering of metered consumption data for residential customers;

5. The proposed program in paragraph 4 together with a program cost estimate shall be filed with the Commission by September 30, 1992;

6. Financial statements and applications for Tariff amendments hereinafter filed with the Commission by the CWC and the system of accounts used by the CWC shall comply, with the necessary changes, with the NARUC Uniform System of Accounts for Class A Water Utilities and shall be presented on a utility basis;

7. The statements under paragraph 6 shall be audited and shall contain a statement from the auditor that they comply with the said Uniform System of Accounts;

8. The requirements in paragraphs 6 and 7 apply to financial statements prepared for the year ending December 31, 1992 and thereafter until otherwise ordered by the Commission;

9. The new rates of depreciation proposed by the CWC in this application are, at this time, denied;

10. Pending the outcome of a Commission-sponsored depreciation study, the CWC shall use classified or individual rates of depreciation;

11. For the purposes of paragraph 10, the classified or individual "1979" depreciation rates are to be used;

12. The proposal of the CWC to calculate depreciation expense on a net-asset basis is approved;

13. The debt interest expense of $245,595 proposed by the Applicant is allowed;

14. The 'Shortfall Recovery Expense' of $108,000 proposed by the Applicant is disallowed;

15. The Commission hereby establishes a target debt interest coverage ratio for the Charlottetown Water Commission in the range of 1.30 to 1.35;

16. This target ratio is be reviewed from time to time and will be adjusted by the Commission where deemed necessary;

17. The allowable rate of return on rate base for the Charlottetown Water Commission is established at 7.07%;

18. All future rate filings of the Charlottetown Water Commission shall include a detailed expense forecast with written evidence describing the budgeting process and the specifics of each budget item;

19. Operating, maintenance and administration expenses in the test period totaling $1,993,698 are allowed;

20. The Applicant's use of the base-extra capacity method of cost allocation is accepted;

21. The application to directly charge customers with unmetered fire lines is dismissed;

22. Except as provided in paragraph 21, all other rate design proposals of the CWC are approved;

23. The CWC shall file with the Commission, on a triennial basis, detailed financial and rate information;

24. Details of the form and content of the filings to be made under paragraph 23 will be provided by the Commission to the CWC at a later date;

25. The first filing under paragraph 23 shall be submitted to the Commission by July 31, 1994;

26. The CWC shall forthwith prepare and file with the Commission for review and final approval a Tariff that reflects the findings and conclusions contained in the annexed Reasons for Order;

27. The Tariff filed under paragraph 26 shall bear an effective date of April 15, 1992 and shall, on the final approval of the Commission, be effective for bills issued on and after April 15, 1992; and

28. Filings made under paragraphs 26 and 27 shall be in written and electronic form and shall contain revenue confirmation calculations and a statement that the filings comply in all respects to the findings and conclusions of the Commission.

DATED at Charlottetown, Prince Edward Island, this 29th day of April, 1992.

BY THE COMMISSION:

Linda Webber, Chairman

John L. Blakney, Vice-Chairman

Michael Ryan, Commissioner

1 The Hillsborough Development, so-called, includes the Community of Hillsborough Park and portions of the Communities of Sherwood and East Royalty.

2 Exhibit A-1, pp. 17-20.

3 Exhibit A-1, p. 25.

4 Unaccounted-for water.

5 Exhibit A-1, p. 30.

6 Tables are derived from Exhibit A-1.

7 Summation, p. 21.

8 Phillips, Charles F., Jr., The Regulation of Public Utilities, (Arlington Va: Public Utilities Reports Inc. 1988), pp. 206-208.

9 Bonbright, James C., et al, Principles of Public Utility Rates, (Arlington Va: Public Utilities Reports Inc. 1988), p. 9.

10 Suelflow, James E., Public Utility Accounting, Theory and Application (East Lansing Michigan: MSU Public Utilities Studies 1973) p. 87.

11 Exhibit A-1, pp. 61-62.

12 American Water Works Association, Manual of Water Supply Practices - Water Rates Manual M1 (New York: American Water Works Association 1983) p. 2.

13 Ibid. p. 3.

14 Ibid.

15 Hay, Leon E. et al, Water Utility Accounting (New York: American Water Works Association and Municipal Finance Officers Association, 1970, Revised 1989) p. 82.

16 National Committee on Governmental Accounting.

17 Hay, op. cit. pp. 80-81.

18 Exhibit I-3, pp. 5-6.

19 National Association of Regulatory Utility Commissioners.

20 Exhibit A-1. p. 62.

21 Re Town of Summerside Electric Department, Order No. E880324 in Docket E-3-1(H) (PEI Public Utilities Commission, March 1988), pp. 8-9.

22 Exhibit A-2, p. 8 of 17.

23 Exhibit A-2, p. 3 of 17.

24 Re Town of Kingsford Heights, (Indiana Public Service Commission,) 83 PUR 4th (1987), pp. 318-319.

25 See, for example, Re Generic Hearing Concerning Accounting and Financial Policies of the New Brunswick Electric Power Commission, Decision, (New Brunswick Board of Commissioners of Public Utilities, May 22, 1991); Re Reference from the Minister of Energy Respecting Ontario Hydro's Proposed Electricity Rates for 1991 - Review of Ontario's Net Income Policy, Report H.R. 19-II, (Ontario Energy Board, January 31, 1991); Re City of Burlington Electric Light Department, (Vermont Public Service Board), 43 PUR 4th (1981), 303; Re City of Bogeman, (Montana Public Service Commission) 18 PUR 3rd (1957), 180.

26 Sprinkler system connections or private fire hydrants.

27 Exhibit P-2, pp. 1-2.

28 Exhibit A-3, Letter to CWC General Manager from City Administrator.